In the Autumn 2015 budget, the Chancellor George Osborne announced that he was going to levy an additional charge of 3% for second homes.

Read - Buying and Selling Property Checklists

This was a new idea and as a result had to go to consultation. I took some time before contributing as I had some real concerns that some people – who had no choice but to have a second home – would get caught up in it.

I wasn’t the only one worried about this and I’m pleased to say that some changes have been made since the consultation concluded so, although not taking everything on board, the government has listened.

To help, the government has now updated its calculator:

Stamp Duty Land Tax Calculator

The key change for the 3% stamp duty for second homes from the original proposal is the timeframe for selling a main residence and buying a new one.

So:

Instead of 18 months, you now have 36 months – ie, three years – to claim a refund of the higher rate. Sadly you still have to pay it initially, which for me is a nightmare scenario!

If you inherit 50% or less of a property, then it won’t be classed as a second home.

The government will apply the 3% to large and small landlords.

Married couples who are considered to be living apart now and in the future will be treated as if they were divorced – a good move, but open to abuse I think!

Other applications/exemptions are as follows, taken exactly from the government document if in italics:

Doesn’t apply to purchases under £40,000, houseboats, caravans or mobile homes.

Interestingly for investors, “the higher rates will not apply to purchases of non-residential or mixed use properties”.

“Where contracts were exchanged on or before 25 November 2015 and the purchase completes on or after 1 April 2016 the higher rates will not apply.” (Although check this with your legal company.)

“An individual buys a plot of garden land from their neighbour. The purchase does not include an interest in one or more dwellings. The higher rates will not apply.”

“The higher rates will not normally be charged on purchases that are charged at the 15% rate for purchases of higher threshold interests in dwellings by companies.”

To be honest, having read the 29 pages on the new rules and all the different scenarios, it’s fairly straightforward if you are clearly buying for investment purposes and already have a main residence.

Read - Buying and Selling Property Checklists

However, if you are in a situation that ends up with you owning two properties for a reason other than investment, such as living in two different places or if you have formed more than one household for any reason, it gets complicated!

Some HMRC examples of who does/doesn’t pay

Example 1:

An individual buys a dwelling and intends it to be her main residence. The effective date of the transaction is 31 May 2019. If she had previously sold a dwelling at any time on or since 1 June 2016 then the purchase may be a replacement of a main residence.

The dwelling she disposed of would have had to have been her only or main residence at some time during the period 1 June 2016 to 31 May 2019. She must not have acquired another new main residence after the disposal and before the purchase.

If the individual had purchased her new dwelling on 31 May 2018 then the three year time limits would not apply. The dwelling previously disposed of by her must have been her only or main residence at some time. She still must not have acquired another new main residence after the disposal and before the purchase.

Example 2:

An individual purchases a new main residence on 30 April 2018 and retains his freehold in the previous main residence at the end of the day of purchase whilst seeking a sale. He meets Condition C. He has not previously sold a main residence, so does not meet Condition D at the date of the transaction.

The transaction is charged at the higher rates.

If he sells his previous main residence at any time during the period to 30 April 2021, then the purchase will cease to be a higher rates transaction and the purchaser can amend his SDLT return and claim back the additional tax paid.

Filing deadlines

Please note that the SDLT must be filed and paid made within 30 days of the effective date of the transaction - as with other types of SDLT purchases.

More detailed help on the new 3% stamp duty land tax for second homes

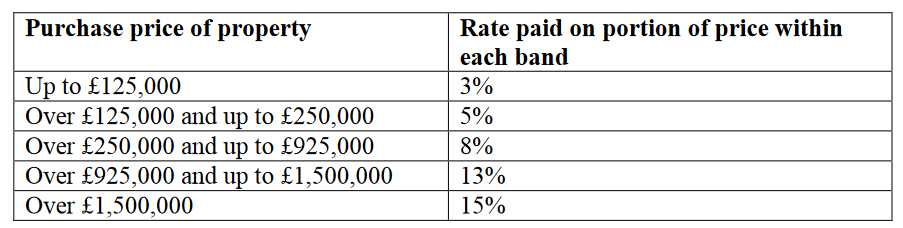

Here’s a handy table to help get to grips with the new 3% rate which is applied on top of the existing stamp duty land tax charged to home owners:

Read - Buying and Selling Property Checklists

How do you claim back the 3% stamp duty land tax?

If you do need to make a claim, then this is how you do it, according to the new rules:

“Repayment can be claimed by completing a SDLT repayment request form. This will be available on gov.uk from 1 April 2016. The form will need to be completed online and the summary printed and posted to HMRC Birmingham Stamp Office.

In due course a form will also be available which can be submitted online. This will require the individual completing the form to verify their identity.”

Here’s the detail of all the 29 pages!

https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/508272/GuidanceNote_Final.pdf