I was on Radio 4 last week to discuss the latest property market news as 2019 gets under way. We talked about the importance of sold property prices data, Brexit uncertainty and the length of time people take to sell their homes.

You can listen back to the show here (I’m on after the first 20 minutes):

Here’s a summary of the interview and more detailed facts and figures!

On average, homeowners in the United Kingdom stay in their home for 19 years, this rises to 23 years in Wales but falls to 15 years in Scotland. First-time buyers on the other hand stay in their homes for about five years whereas those buying later in life will stay put for around 30 years, so this is an ‘average’.

This is why I don't worry so much about year on year price changes when looking at data from a consumer perspective.

For example, if someone bought for the ‘average time people stay in their home’ ie 19 years ago, the 'average' price paid for a property in the UK would be around £84k and it's now worth £231k.

So it’s really irrelevant what happened year on year, as how much your property is worth and whether it’s worth more or less than you bought it for depends on how long you’ve owned it for. For example, if you’d bought at the height of the property market in the UK prior to the crash, you would have paid £189k, so with average prices you would have seen a 22% rise to £231,000.

However, if you had bought at the market low in 2008/9 you would have bought at £154k, so in todays market you would have seen a price rise of double this – 50%!

As a rule of thumb, anyone who has bought since 2013 will have seen some good rises - irrespective of what's happening year on year, as this was the year most areas started to recover prices.

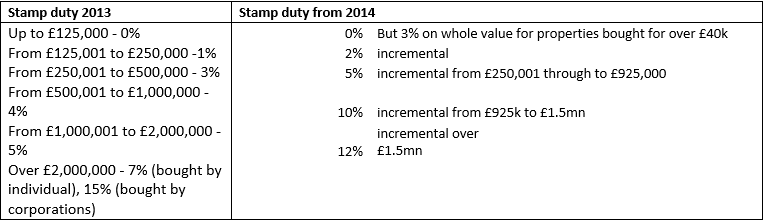

However, there are lots of different property markets, so if you have been working or buying in the Prime Market of London, you would have seen great rises since the credit crunch, but since 2014, due partly to Brexit, but mostly due to the stamp duty tax increases (see chart below), you could have seen falls of 18%!

The key thing is to worry less about what happens price wise and more about:

If something happens, for example, prices do fall, you lose your job, get sick, split up, the question to ask before you buy is “how will you manage?”. If you are never forced to sell and can choose to sell when your property is ‘in profit’ then you don’t need to worry so much about property prices.

Remember, it’s the cost of putting a roof over your head that you should be focusing on and with mortgage rates at an all-time low and 5% deposits available, then this may well be the most cost effective thing to do – irrespective of the property’s value.

Talk to your mortgage broker and insurance contacts about how to protect yourself from price falls and ‘life events’ happening over the next few years as they can help you find strategies to help.

If you are trading down and have lived in their property a long time, perhaps owning it with cash, then worry more about finding the right property for you.

For those trading up the ladder, falling prices can actually be financially beneficial as you can save more money than you lose. Remember, if you are buying your ‘forever home’ prices are likely to rise/fall/stay the same over the next 20 year, so focus on finding a property you love which you can always afford, whatever happens in life or the market.

When buying for the first time, it’s more about making sure you are 100% financially and personally settled. Remember when the credit crunch hit and prices fell by 25%, 95% mortgages virtually disappeared and trying to buy with a 90% LTV was also tough. 50% of first time buyers dropped out of the market, but so did the number of properties for sale too.

So for those ‘hoping’ prices will fall, be careful what you wish for!

And, buying in a ‘less busy’ market that exists now means you don’t have to worry about competing to purchase a property with lots of other potential buyers, which may well happen post Brexit if the market doesn’t take a ‘dive’. And you may even be able to make and get accepted a cheeky offer – saving you money in the long run.

Do though speak to a mortgage broker about how you would cope financially if the property fell into negative equity.

Need more help? Contact us.

| How to secure the right mortgage - Mortgage Advice Bureau | Are you in a buyers' or sellers' market? - The Advisory |

|

|