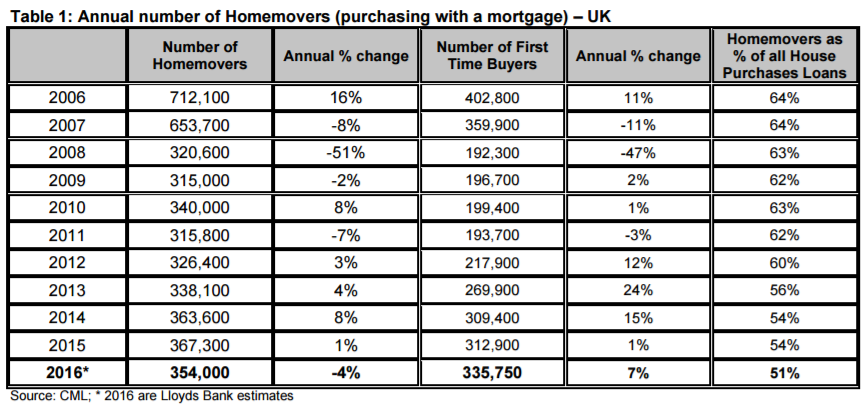

The number of us moving home – with a mortgage – has dropped for the first time in five years, according to research from the most recent Lloyds Bank Homemover Review.

In 2016 the number of homemovers is estimated to have been 354,000, a drop of 4% from 2015. This is the first yearly decline since 2011 after four years of continuous growth.

However, it’s important to remember this doesn’t include data on cash buyers, who account for approximately 30% of the market.

The current number of movers is still more than 10% higher than the lowest level since the crash in 2009, when it was just 315,000; the second lowest figure on record.

However, the 2016 figure is just half the number of movers with a mortgage seen 10 years ago.

Andrew Mason, Lloyds Bank Mortgages Director, said: “Despite favourable economic conditions including record low mortgage rates, high employment levels and rising real pay growth, the number of homemovers fell in 2016 for the first time in five years. Whilst higher prices will have lifted equity levels for many current owners, the low availability of the ‘right type’ of homes for those looking to move up the housing ladder may have constrained market activity. Of course, higher prices may explain why more homemovers are opting for longer mortgage terms.”

Moving home? Here's how to organise your removals.

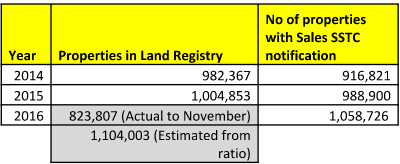

Although Halifax state that the number of people moving with mortgages is down year on year, statistics from View My Chain show that the actual number of sales is up year on year.

The reason for the difference in figures is that the number of cash buyers is approximately 30% of the market as the ‘baby boomers’ are all paying off their mortgages and over 50% of people now own their property outright – with no mortgage at all.

View My Chain which tracks property sales from ‘sold subject to completion’ through to the completed sale shows that the estimated final sales for England and Wales in 2016 is just over 1 million properties, suggesting sales actually rose in 2016 by 7%, so a very different story to mortgaged sales.

There were also less fall throughs in 2016, partly due to the huge upsurge in sales to buy to let investors and second home owners in the first quarter. Sohail Rashid explained in “2015 there were just over 149,000 property sales which fell through, whereas in 2016 it was 109,000”

For more on sale fall throughs visit View My Chain.

Cost for movers is on the up

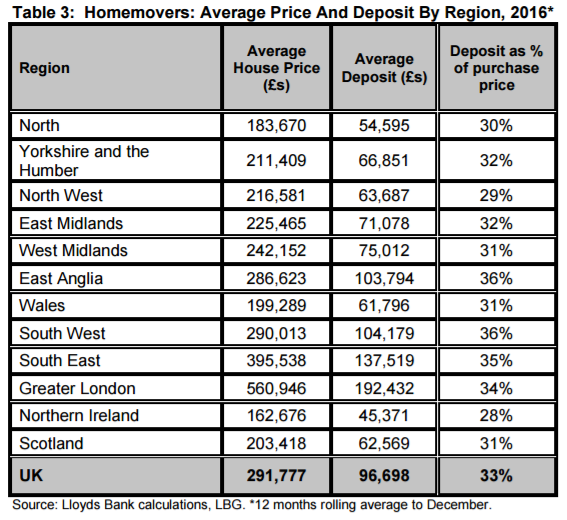

Last year, the average house price for movers went up by 7% to a historic high of just over £291,000.

Since the low of £199,645 in 2009, the price paid by movers has risen 46%. Most regions across the UK have seen prices increase significantly since 2009 – London movers are now paying around £560,000, a record high, although first-time buyers can still secure properties for £105,000.

The only place paying below 2009 levels is Northern Ireland, which has experienced a 3% drop.

Higher prices = higher deposits

For those who do own a home already, higher prices mean they gain equity in their existing property and that typically means they can buy the next one with a bigger deposit. This is reflected in Halifax’s figures which show the average deposit for those who have a home already has risen to £97,000 – up 33% since 2009.

During the last year, deposit levels grew by just over £5,500.

However, what’s important to know is that this doesn’t mean this is the deposit you ‘have to have’ as is often inaccurately reported by the media – and certainly was with this research. Most first-time buyers only need to put down a 5% deposit; the fact they put down more is generally because they can afford to do so, often thanks to the bank of mum and dad.

Some areas are seeing a rise in deposits, Northern Ireland see falls

Four regions in the South of England now have average mover deposits of more than £100,000 and in London that figure rises to around £192,000 to move up the property ladder, up 74% since 2009.

At the opposite end of the scale, movers in Northern Ireland have experienced a 25% drop in deposits in the same time period, with the average now at around £45,000, the nation’s lowest. That’s mainly due to the huge falls in property prices in the region during the credit crunch; they are still 40% lower than they were at the height of the market pre-crash.

Homemovers preferring longer term mortgages

Over the last 10 years, there has been a trend towards longer-term mortgages, with movers choosing loans which go beyond the previously standard 25-year term.

In 2006, 83% of movers had mortgage with a term of 5-25 years; by 2016 this had dropped to 61% with the remaining 39% being made up of mortgage terms of 25-35 years.

This isn’t a surprise. We are living much longer and the pension retirement age is on the up, so as prices rise in some areas and the mortgage market review tightens affordability, it is a natural move to lengthen the term to ease payment costs.

Low rates are keeping mortgage affordability under control

Mortgage rates are at a record low and this has helped reduce payments as a proportion of movers’ real outgoings.

In the final quarter of last year, mortgage payments totalled 38% of movers’ income. This isn’t dissimilar to the long-term average of 40% and is a marked improvement since the summer of 2007 where payments peaked at 57% of disposable income.

Not sure about how to choose a mortgage? Read our securing a mortgage checklist.