Will 2017 be the first time property price inflation starts to match wage growth?

For many years now, property prices have outstripped wage growth with rises across the country since 2000 averaging 6-9% EVERY YEAR.

This has been made possible by:

Studying house price inflation across the country – at individual property and postcode level – has meant I have been able to see vast differences emerging in house price growth. No longer is national or even local property price growth inflation uniform; it is individual to each property or, at best, a street.

Due to substantial shortages in stock available to buy versus demand, property sales in many areas across the country have become ‘auctions’ where people bid up the price as much as they need to secure the home of their dreams.

A property which is popular in a great location could have seen fantastic price growth, while one down the road in not such a good area, with a poor layout, may experience growth at a fraction of the rate, or even non-existent.

As a reminder of this, here’s the BBC report we did on Peterborough which shows exactly what I mean:

From a rental perspective, this hasn’t quite happened yet. In fact, rental inflation is on average in line with wage growth; around 2% each year, according to the ONS. Unfortunately, poor government policies over the last 25 years are now likely to curb the growth in stock in the private rented sector which means it is quite possible we will see rental inflation outstripping wages in the coming years.

That’s why the likes of economic success stories such as London, Cambridge, Bristol, Harrogate have seen property prices outstrip wage inflation, while areas which have experienced economic decline, such as Merthyr Tydfil and parts of Sunderland, have hardly moved at all since 2004.

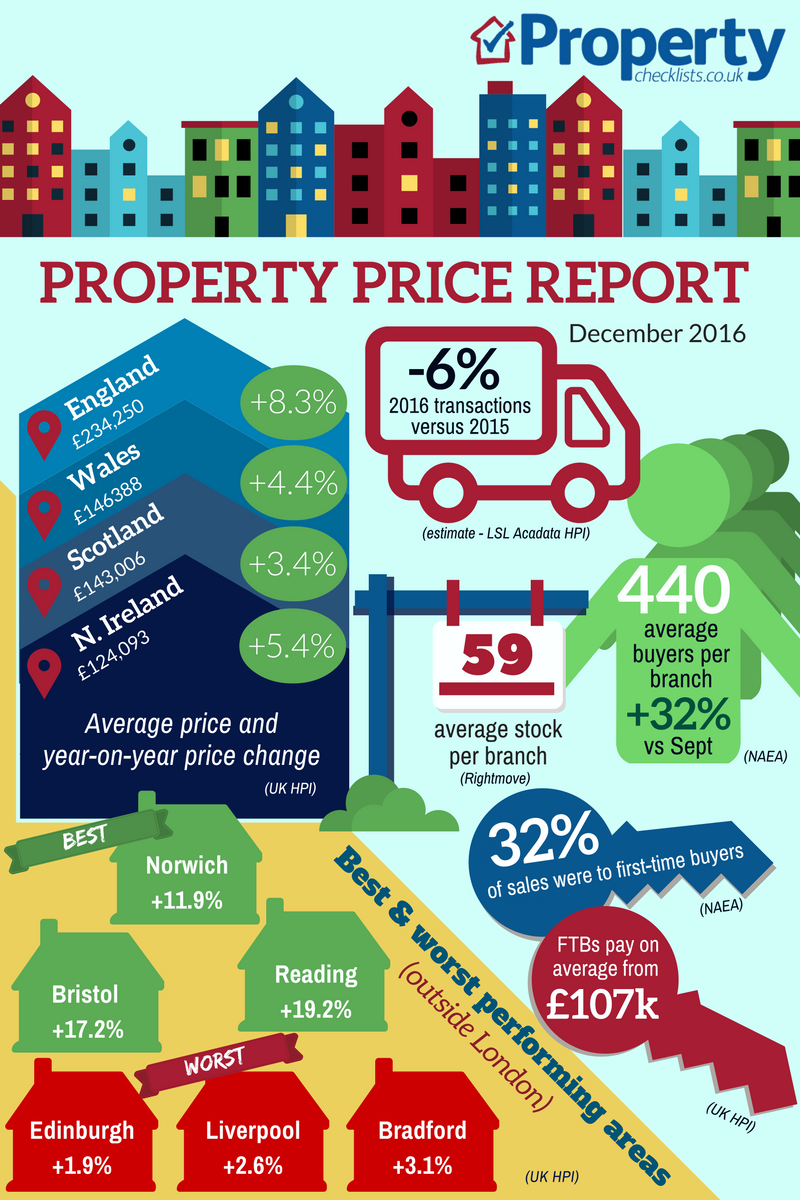

What's the story with property prices?

UK, England and Wales data

Key facts:

Average prices across the indices vary from mortgaged only prices from the Nationwide HPI (Nov 16) of £204,974, through to marketing prices (ie not necessarily sold) from Rightmove (Oct 16) of £305,670, a 49% difference. Average sold prices from the UK HPI stand at £234,250 (Sep 16).

The market is definitely softening as expected and many agents are now looking at 2017 as being a quieter year from a transaction perspective. No more major policy changes (we hope!) are expected next year that will affect the market, such as increases in stamp duty or Brexit votes. However, it’s likely that attention will turn to the private rented sector instead when landlords potentially start to realise buy-to-let investment is going to be increasingly tough to make stack up financially. This is likely to have a positive and negative effect on some areas – some landlords may sell, boosting transactions in the short term – while in others, we may just see fewer buyers, keeping property price inflation in check versus the 4-6% increases we have been seeing over the last few years.

Are you looking to sell? Read our expert quick guide.

For more, download my comprehensive property price report.

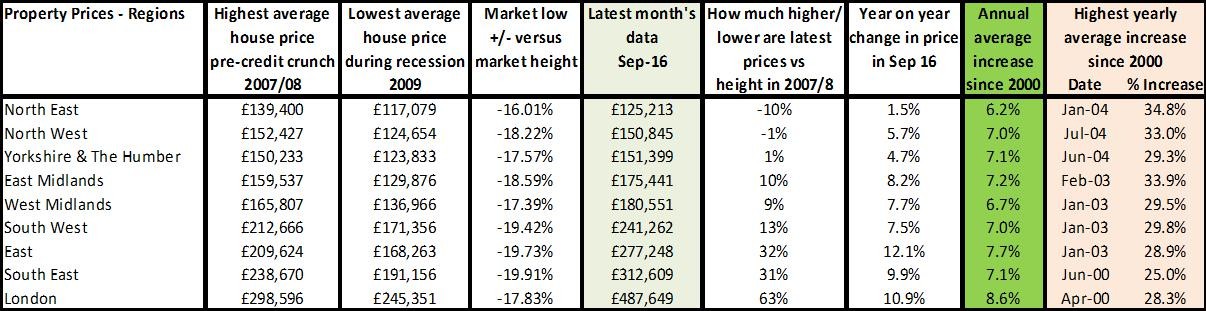

What's happening in the regions?

Source: UK HPI

It’s interesting when you average out year-on-year changes since 2000, most areas/towns have shown annual growth rates of 6-8.6%, according to the government’s HPI index. But when you take into account property prices over the last 11 years – ie from 2005 – annual growth has almost halved from these levels. This suggests perhaps that at last property market price inflation will stop beating income growth. This should come as no surprise as it’s likely due to the government restricting lending levels at 4.5 times incomes and making affordability tougher with the Mortgage Market Review rules. Although this may dampen the market in the short term – and all the forecasts suggest 2017 won’t be a good year and may even see some price falls – it is good news in the long run as the only way people can continue to transact in the property market is if prices are maintained at a more affordable rate.

Confused about mortgages? Here's how to secure the right one for you.

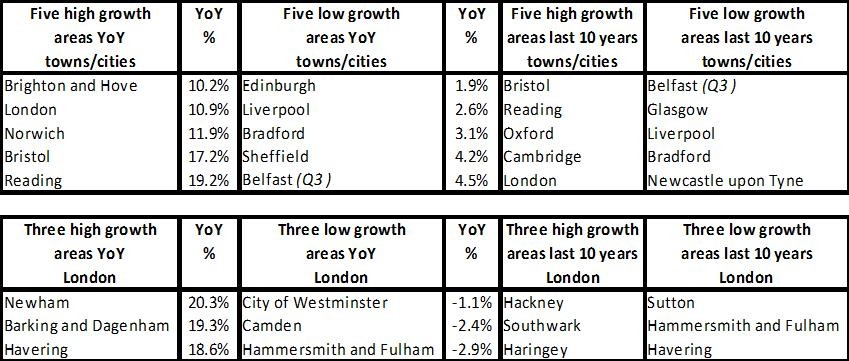

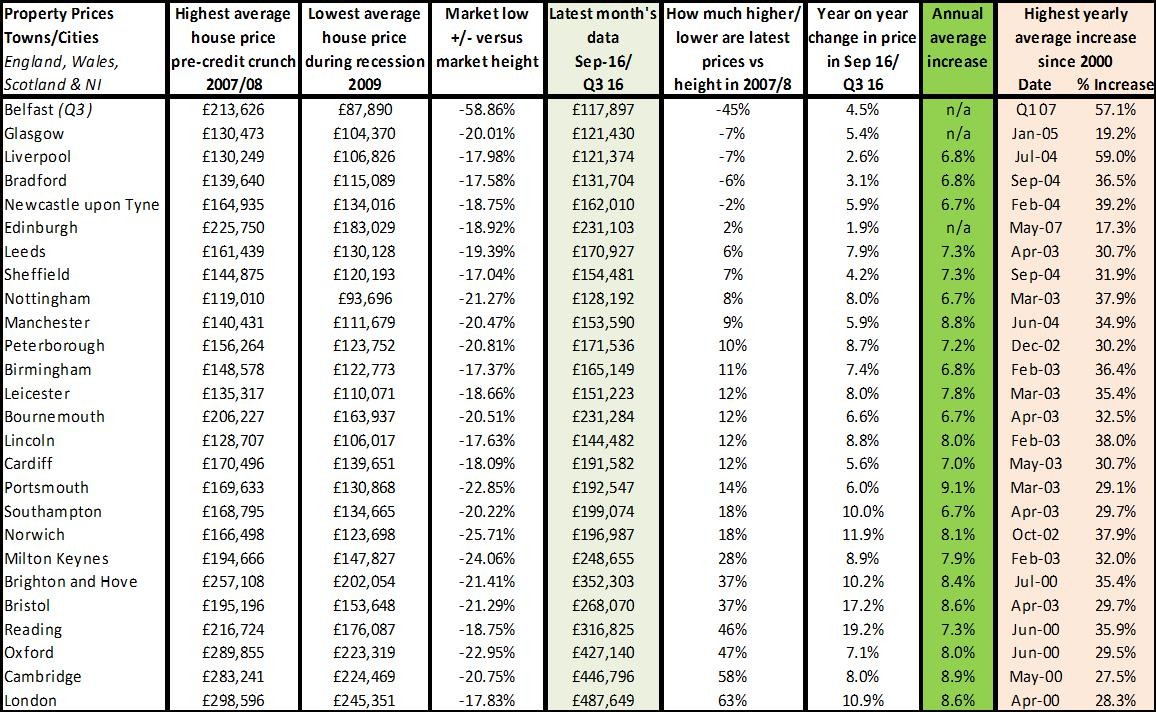

What's happening in your town or city?

Source: UK HPI

Although nationally and regionally the property market seems to ‘make sense’ from a trend, economic and policy perspective, it’s the local demand and supply factors which are impacting dramatically on the huge variations seen when looking at towns’ and cities’ year-on-year growth. For example, Edinburgh is seeing the lowest growth of 1.9% year on year, while Reading is maxing out growth at 19.2% versus 2015.

From an agent perspective, this means it is important to work with the local media and public to ensure they understand what’s happening nationally and regionally and that this could be incredibly different at a local level. Indeed, in areas such as Belfast and Bradford, many homeowners’ property values could still be less than they paid while people in other areas may have bought at the low of the market and now be well off enough to move up the ladder to their next home.